- Monday - Saturday 10:00-19:00

- (+91) 9319938833

- info@aaavaluation.in

P&M Valuation Experts with experience over 35 Years.

Background an experience to handle such assignments for all assets classes

Beginning of AAA Group

Beginning of AAA Group,

when our Chairman, CA. Anil

Goel founded the CA Firm

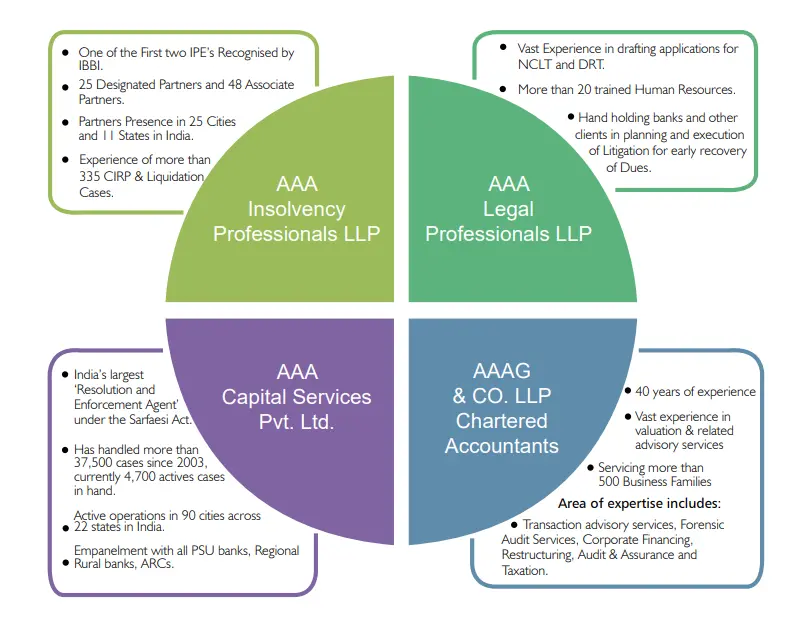

Incorporation of AAA Capital Services Pvt Ltd

Incorporation of AAA Capital

Services Pvt Ltd for providing

services relating to financial

Advisory and Corporate Debt

Structuring Services.

Handled 27,500 Cases.

AAA Capital Services Pvt Ltd

started operations as enforcement

agent under SARFAESI Act. Since

then the company has handled

more than 27,500 Cases.

AAAG & CO LLP

AAAG & CO LLP, with its vast

experience in preparing Bank Loan

Proposals and Loan Syndication,

made quick inroads in Valuation of

Shares required under FEMA &

Companies Act